Fidelity to charge up to $100 ETF fee for nonpaying sponsors

Fidelity will charge a 5% transaction fee, capped at $100 per buy order, on ETF purchases where sponsors do not pay a direct asset-based fee, effective June 1.

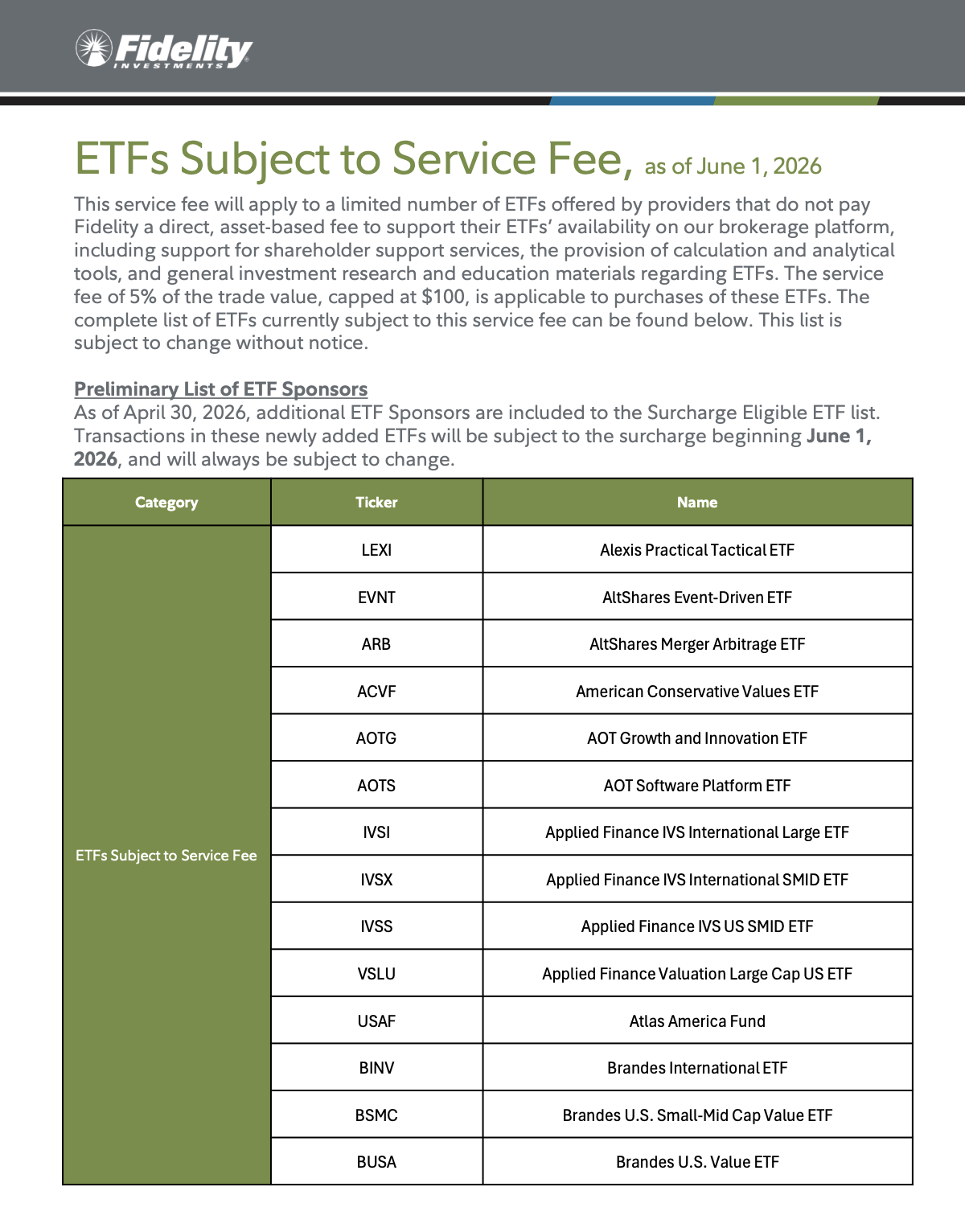

Fidelity will begin charging a 5% transaction fee, capped at $100 per client buy order, on purchases of exchange-traded funds whose sponsors do not pay a direct, asset-based fee. The change takes effect June 1 and was disclosed to registered investment advisers and wealth firms in a document that lists ETFs currently subject to the charge.

Fidelity’s notice says revenue from sponsors will “support their ETFs’ availability on our brokerage platform, including support for shareholder support services, the provision of calculation and analytical tools and general investment research and education materials regarding ETFs.” The company added the list of affected ETFs is subject to change without notice. The fee applies to each client buy order for participating ETF products.

Fidelity Institutional Wealth Management Services, which manages the company’s clearing and custody operations, provided prepared statements to clients rather than in-person interviews. Steve Richard, who became head of the business in January, wrote in a prepared statement that Fidelity has been a provider of clearing and custody services for more than four decades and that the firm uses its scale to help clients grow. Trevor Norton, head of custody for RIAs and family offices, described the firm’s approach as relationship-based pricing and noted clients consider total cost of ownership when selecting a custodian.

Custodians generate revenue from transaction fees paid by investors, payments from fund companies for product distribution and servicing, and interest income from cash and securities lending. Industry consultants note that as investor flows shift from mutual funds to ETFs, those revenue dynamics have changed and large custodians are seeking more direct compensation from ETF sponsors.

Tim Welsh, founder of consulting firm Nexus Strategy, said service capabilities remain a key advantage for large custodians when advisors evaluate platforms. “There’s no exclusivity anymore in terms of, ‘Hey, we’ve got cool products.’ It’s all now about service,” he wrote in comments provided to Fidelity clients.

Fidelity’s custody business administers about $5.5 trillion in assets for roughly 3,300 RIAs and other wealth firms and the larger company processes about 5.5 million trades daily across dozens of markets and currencies. Unlike one rival that publishes pricing for some custody services, Fidelity does not publish a listing of starting prices for clearing and custody contracts.

Other major custodians have also introduced fees tied to ETF servicing, and analysts have recommended servicing fees and revenue-sharing as levers to strengthen platform profitability. Devin Ryan, an analyst at Citizens Bank, noted in a research note that ETFs represent a visible near-term lever for custodians to boost revenue.

Some advisory platforms use multiple custodians. Trey Prescott, director of business development at Advisory Services Network, recalled that Fidelity was the first custodian to accept ASN when the platform had few assets and remains a major provider for the firm.

Fidelity provided the disclosure to its clearing and custody clients and answered questions in writing. The list of ETFs subject to the fee and the terms of sponsor arrangements are negotiable and may change over time.

Tags

Articles by this author