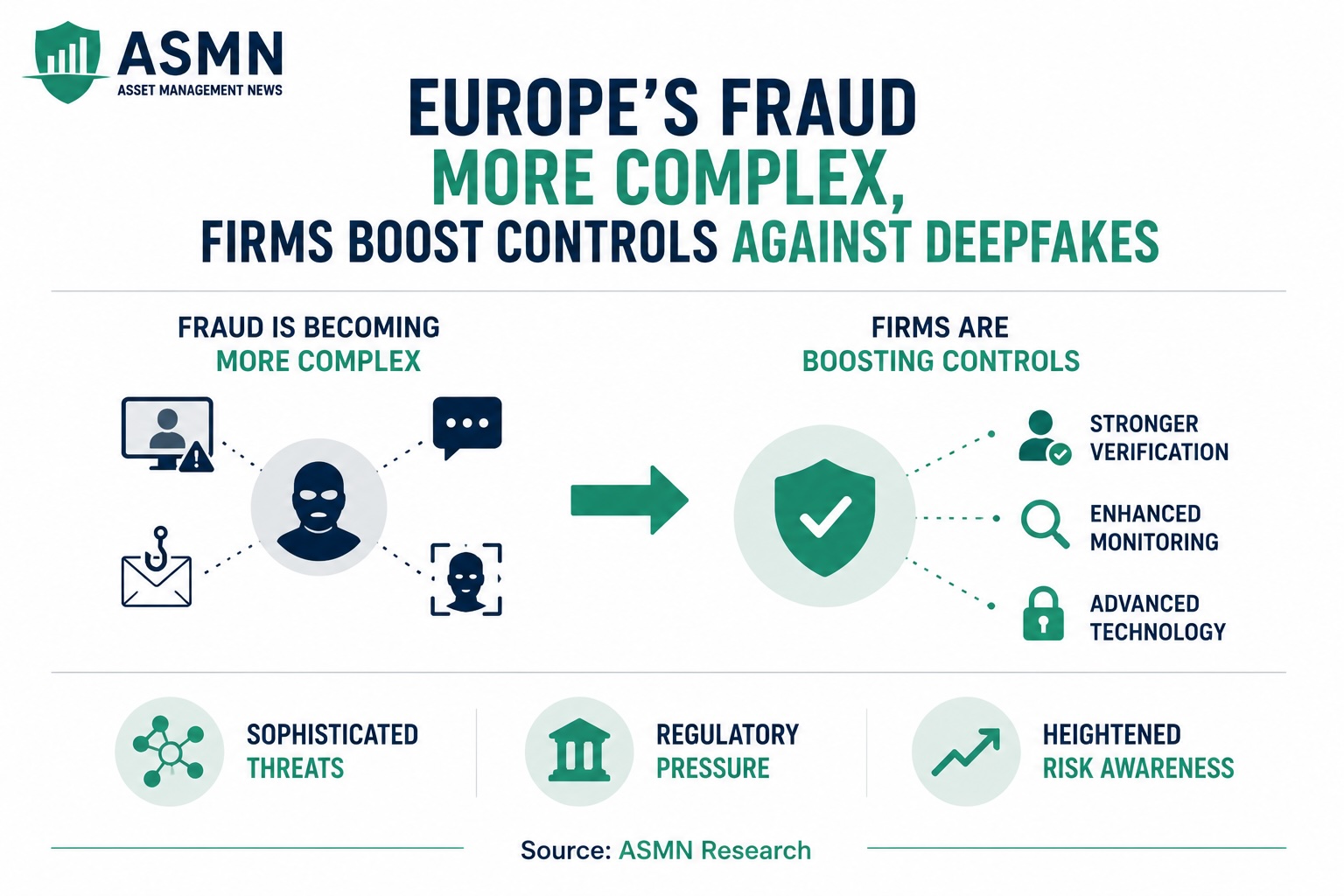

Europe’s fraud grows more complex; firms step up controls

Banks, payment firms and authorities report more sophisticated fraud using synthetic identities, deepfakes and crypto, prompting real-time monitoring and wider cross-border cooperation.

Banks, payment firms, retailers and law enforcement across Europe report a rise in increasingly complex fraud schemes over the past several years, driven by digital payments and remote onboarding.

Criminals are using combinations of synthetic identities, account takeover, deepfake-assisted social engineering and cryptocurrency channels to move money and hide its origin. Incidents have been reported in multiple member states and often involve perpetrators and victims in different countries.

Industry sources point to several factors behind the shift. The move to online banking and e-commerce increased remote account openings and contactless payments. Wider use of instant payment systems and real-time transfers gives criminals faster ways to move funds. Automated bots, encrypted messaging and readily available anonymizing services enable organized groups to scale operations. Cryptocurrencies are being used for layering and laundering because some flows are harder to trace than traditional channels.

Financial institutions and public agencies identified recurring patterns. Authorized push payment scams involve customers being tricked into approving transfers to accounts controlled by criminals. Synthetic identity fraud combines real and fabricated information to open accounts that pass basic checks. Invoice fraud and business-email compromise target companies with tailored requests to reroute payments. Several banks reported multi-stage attacks that start with small test transactions before escalating.

Regulators and compliance teams say recent security measures have lowered some types of card and authentication fraud, but criminals have shifted to other vectors. Firms report gaps in cross-border data sharing, uneven enforcement across jurisdictions and limits on rapid information exchange as obstacles to stopping fast-moving scams.

Banks and payment providers are expanding technical controls and cooperation. Firms are investing in real-time transaction monitoring, behavioral analytics and stronger identity checks at onboarding. Many are deploying machine-learning models to flag unusual patterns and pairing automated alerts with human review for high-risk cases. Financial intelligence units and law enforcement units report increased engagement with the private sector to trace suspicious flows and freeze funds more quickly.

A senior compliance officer at a large European bank noted that criminals combine established techniques with new technology, making faster detection and closer cooperation necessary. An EU regulatory official stated that improving automated information sharing across borders and sectors is a priority for upcoming workstreams.

Legal and policy constraints affect responses. Data protection rules, differing national reporting standards and fragmentation in anti-money-laundering regimes limit rapid cross-border collaboration. Regulators are working on harmonization and new standards to improve traceability of funds and extend compliance obligations to some crypto service providers, but implementation timelines vary by country.

Firms and authorities say planned actions focus on faster detection, better data sharing and tighter controls for remote transactions. Specific initiatives and schedules differ across member states.

Tags

Articles by this author