Europe fraud surge pushes firms, regulators to tighten controls

Fraud in Europe has become more complex since 2020, prompting banks, fintechs and EU regulators to tighten payment, identity and cross-border reporting controls.

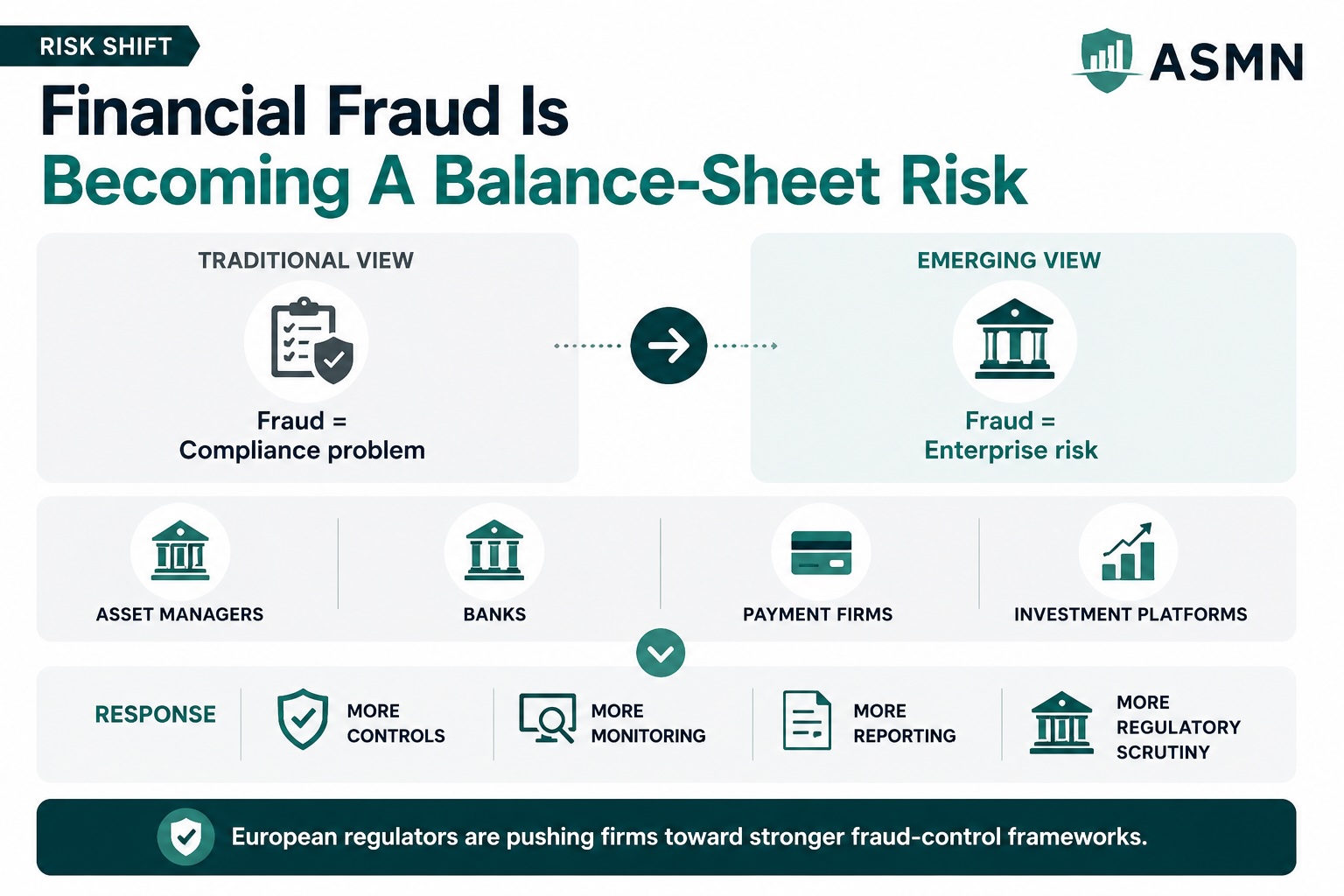

Since 2020 fraud across Europe has grown more complex, pushing banks, payment processors, retailers and fintech firms to strengthen controls on payments, identity checks and cross-border reporting.

Firms report increases in schemes that combine technology with social engineering, including account takeover, card-not-present fraud, invoice and business email compromise and scams tied to cryptocurrencies.

Growth in online commerce and new financial technologies expanded targets and tested authentication systems. Criminal groups use automation, bots and stolen or synthetic identities to scale attacks quickly across national borders.

European regulators have updated rules and published guidance. Strong Customer Authentication under PSD2 reduced some card fraud but gaps remain in remote onboarding and merchant-side controls. The Digital Operational Resilience Act and NIS2 impose new cybersecurity and incident-reporting requirements for the financial sector. Revisions to anti-money laundering rules and proposals for faster information sharing aim to limit movement of illicit proceeds across jurisdictions.

Companies report wider use of behavioural analytics and machine learning to detect anomalous transactions, along with transaction velocity checks and tougher KYC and KYB procedures for customers and suppliers. Payment processors and banks are expanding monitoring for mule networks and suspicious account openings and are tightening authentication flows for high-risk transactions.

Industry groups are promoting standardized data formats for fraud alerts so banks and law enforcement can act faster. Private executives and compliance officers have asked for quicker sharing of indicator-of-compromise data between firms and with authorities to block attacks earlier.

Cross-border investigations face obstacles because enforcement rules and capacity differ by member state. Law enforcement officials note many rings operate across countries, using servers, money mules and conversion services in multiple jurisdictions, which slows takedowns and complicates recovery of stolen funds.

Smaller firms and non-financial businesses that now handle payments are reporting greater exposure. Retailers, marketplaces and service providers without dedicated fraud teams face higher chargeback costs and operational losses and are turning to third-party fraud monitoring and identity verification vendors.

Financial institutions are signing information-sharing agreements and joining public-private task forces to coordinate responses to new scams. Regulators are urging rapid incident reporting and baseline controls for remote onboarding and transaction monitoring. Industry specialists recommend regular fraud risk assessments, stricter supplier checks and clear incident response plans that involve relevant authorities.

Payment rails, open banking APIs and faster cross-border transfers have increased convenience and widened the attack surface. Criminals combine conventional fraud techniques with automated tools and synthetic identities constructed from fragmented personal data. Authorities have called for tighter corporate controls, closer regulatory oversight and improved information sharing to reduce safe havens for criminal networks.

Tags

Articles by this author