Diageo, Heineken and AB InBev face falling alcohol demand

Younger consumers drink less, inflation hits discretionary spending and health tech alters habits, reducing demand for beer, wine and spirits at major alcohol firms.

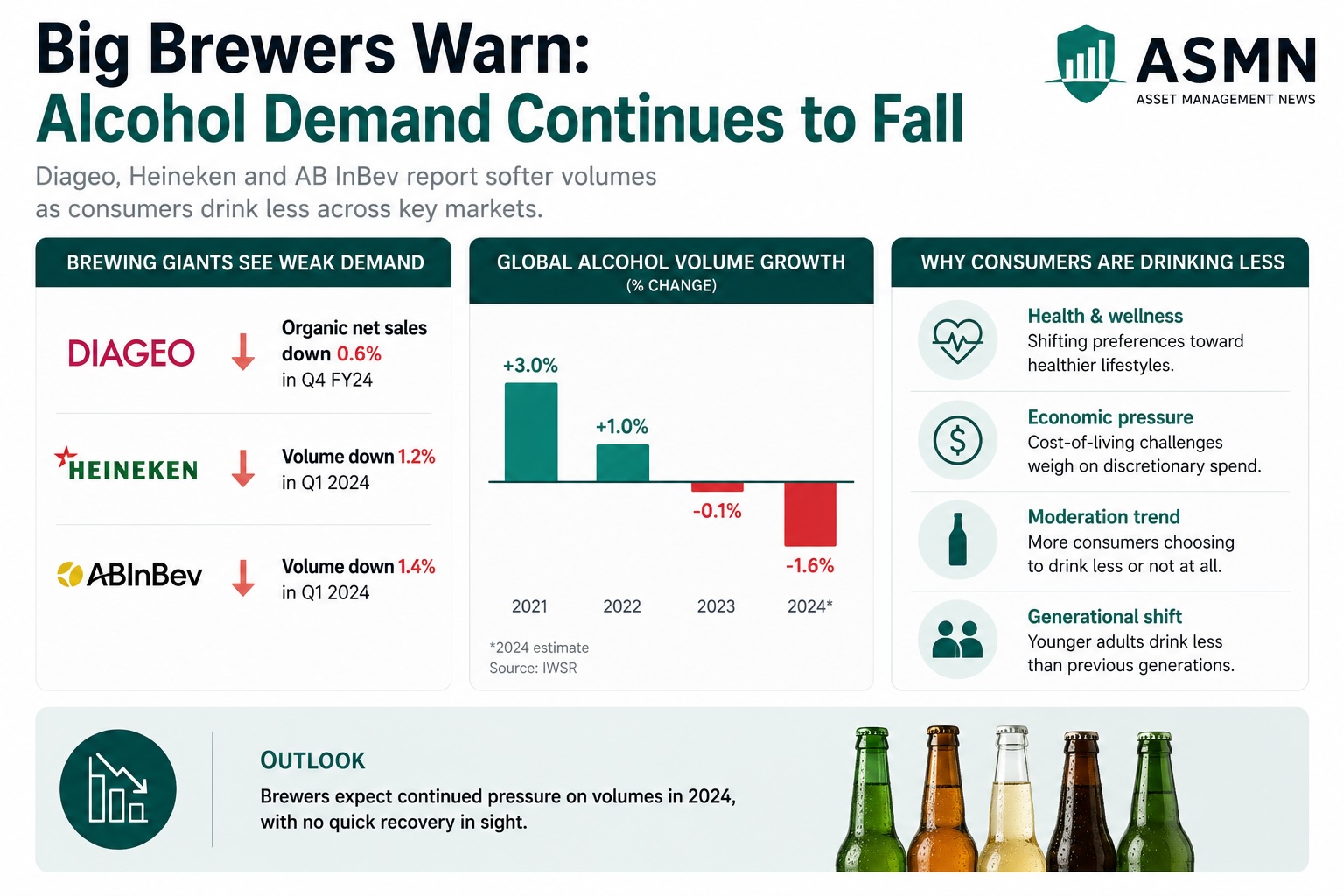

Diageo, Heineken and Anheuser‑Busch InBev are reporting weaker demand for beer, wine and spirits as younger cohorts drink less, prices rise and health and technology trends change behaviour.

Public health data show rates of lifetime, past‑year and past‑month drinking among young people have declined since about 2000. BNP Paribas chief investment strategist Stephan Kemper estimates roughly 36% of Gen Z now identify as non‑drinkers and says people who do not start drinking in early adulthood are unlikely to take it up later.

Economic pressure has reduced occasions for drinking out. US inflation rose to 4.2% in May, a three‑year high, and lower consumer confidence has encouraged households to cut back on social activities where alcohol consumption is concentrated. Companies report pandemic‑era changes to socialising have persisted alongside the cost‑of‑living squeeze.

Health monitoring tools and new medicines are cited as additional influences. Analysis of about 30,000 new users of a biometric wristband over 72 weeks found self‑reported drinking days fell from 23.0% to 17.2% of days, with reported alcohol volume also down. Amanda Wick, principal at Incite Consulting, noted: “Alcohol’s effects become immediately visible rather than abstract.” Oura has sold about 5.5 million rings that track sleep and activity. Analysts also point to GLP‑1 weight‑loss drugs such as Ozempic; Morgan Stanley projects the global market for weight‑loss and obesity treatments to grow from $79 billion in 2025 to $190 billion by 2035.

Firms are responding by emphasizing premium products and expanding no‑ and low‑alcohol ranges. Brands launched alcohol‑free versions including Budweiser Zero, Corona Cero and Michelob Ultra Zero, plus 0% editions of some Guinness, Tanqueray and Gordon’s labels. AB InBev has reduced the number of actively marketed labels in many markets to three to five “megabrands,” increasing those brands’ share of marketing spend to about 70% from about 50% in 2021.

Performance across the sector has varied. Diageo’s share price has fallen more than 19% in the past year and the company reported a 9.4% decline in North American sales in its third quarter. Anheuser‑Busch InBev’s stock rose about 13% in the last year, but its US depository shares returned roughly 7% over five years and global beer volumes declined about 2.6% in 2025. AB InBev posted a quarter of 0.8% volume growth aided by price increases, while North American volumes fell 3.1% and regional sales rose 0.9%. Diageo replaced its chief executive in 2025, appointing Dave Lewis.

Analysts estimate the sector has lost more than $800 billion of market value in recent years and say the valuation gap with broader markets is at a multi‑year high. Some mature markets show weak volume growth while parts of emerging markets recorded increases: between 2024 and 2025 South Africa’s beverage alcohol volume rose about 4% and value about 12%, while India posted roughly 4% volume growth and 5% value growth in the same period.

Short‑term events can lift sales. Investment bank estimates indicate a global football tournament could add about one billion extra pints and raise global beer volumes by around 0.3% in a World Cup year; host nations can see higher local gains. Companies with sponsorships and strong exposure in host regions, including AB InBev and Heineken, are expected to benefit from those events.

Companies have introduced product innovations and reshaped portfolios in response to the changes in drinking patterns. Analysts report those measures are intended to offset weaker volumes and to support margins and pricing, while acknowledging near‑term boosts from major sporting events.

Articles by this author