Autocallable ETFs: how they deliver yield and risk

Solactive CMO Timo Pfeiffer told Off the Record that autocallable ETFs use bank notes via swaps and index rules to target 8–10% yield but can lose value if the underlying drops about 30–40%.

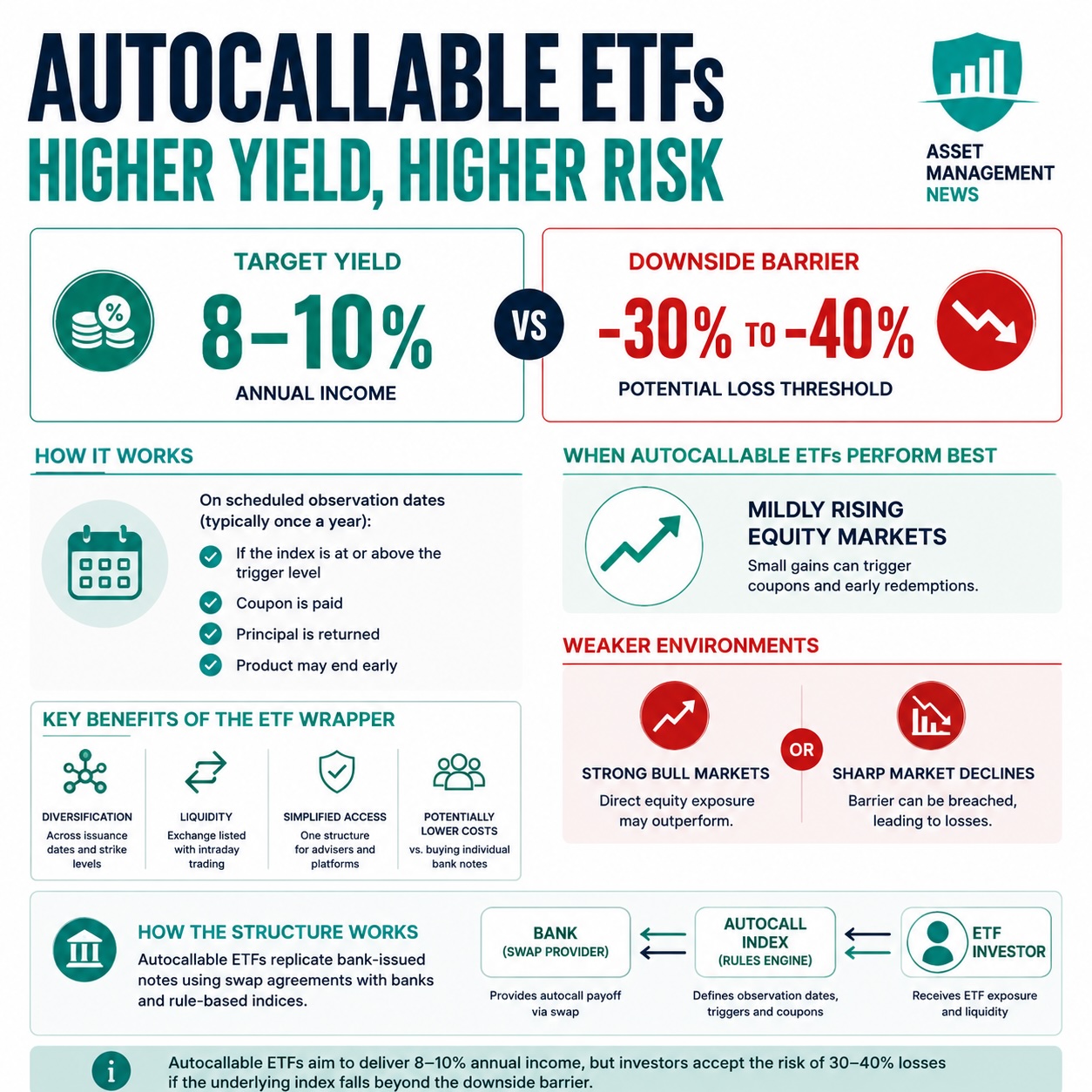

Timo Pfeiffer, chief marketing officer at Solactive, described autocallable ETFs as funds that replicate bank-issued autocall notes using swap agreements and rule-based indices. The structures aim to pay higher annual income, commonly around 8–10%, while exposing investors to large losses if the underlying index falls past a preset barrier, often in the 30–40% range.

The funds follow a set schedule of observations, usually once a year. If the index is at or above the trigger level on an observation date, the product can pay principal plus the coupon for the period and end early. If the trigger is not met, the strategy continues to the next observation, typically until a multi-year maturity such as five years.

Issuers generally do not place individual structured notes inside the ETF. Instead, they enter swaps with banks that provide the autocall payoff profile. An index defines the observation dates, trigger rules and coupon calculations, and automates monitoring and rebalancing. Pfeiffer described the index as “the engine behind it.”

Pfeiffer said the autocallable ETF trend started in the United States about a year earlier and has spread to Canada and Europe. He cited the wider option-based ETF category at roughly $300 billion in assets and noted individual large products that have tens of billions. By comparison, banks issued about $140 billion of autocall notes in 2025, while assets in autocallable ETFs remained on the order of a few billion dollars.

The ETF wrapper changes the investor experience compared with buying single bank notes. A fund can spread exposure across issuance dates and strike levels, offering diversification versus selecting one of thousands of listed notes. ETFs provide exchange listing and intraday liquidity and present a single regulatory and operational structure that advisers and platforms can use more easily. Pfeiffer noted retail investors in some markets face thousands of individual autocall listings; he gave about 15,000 as an example for Germany.

Autocallable ETFs tend to perform best in mildly positive equity markets, where small gains trigger coupons and early redemptions. In a strong bull market, a direct equity allocation can outperform. A sharp market drop that breaches the downside threshold will produce losses for holders. Pfeiffer warned, “There is a downside risk that you are accepting.”

Historically, structured autocall notes were sold through retail channels, private banks and wealth managers. The ETF format may broaden access by simplifying distribution and lowering per-investor costs, but tax rules and market structure differences between regions will affect adoption. Pfeiffer also said the approach could be applied to other underlyings over time, though equity indices are likely to remain the largest share.

Articles by this author