AI, reshoring drive U.S. electricity demand rebound

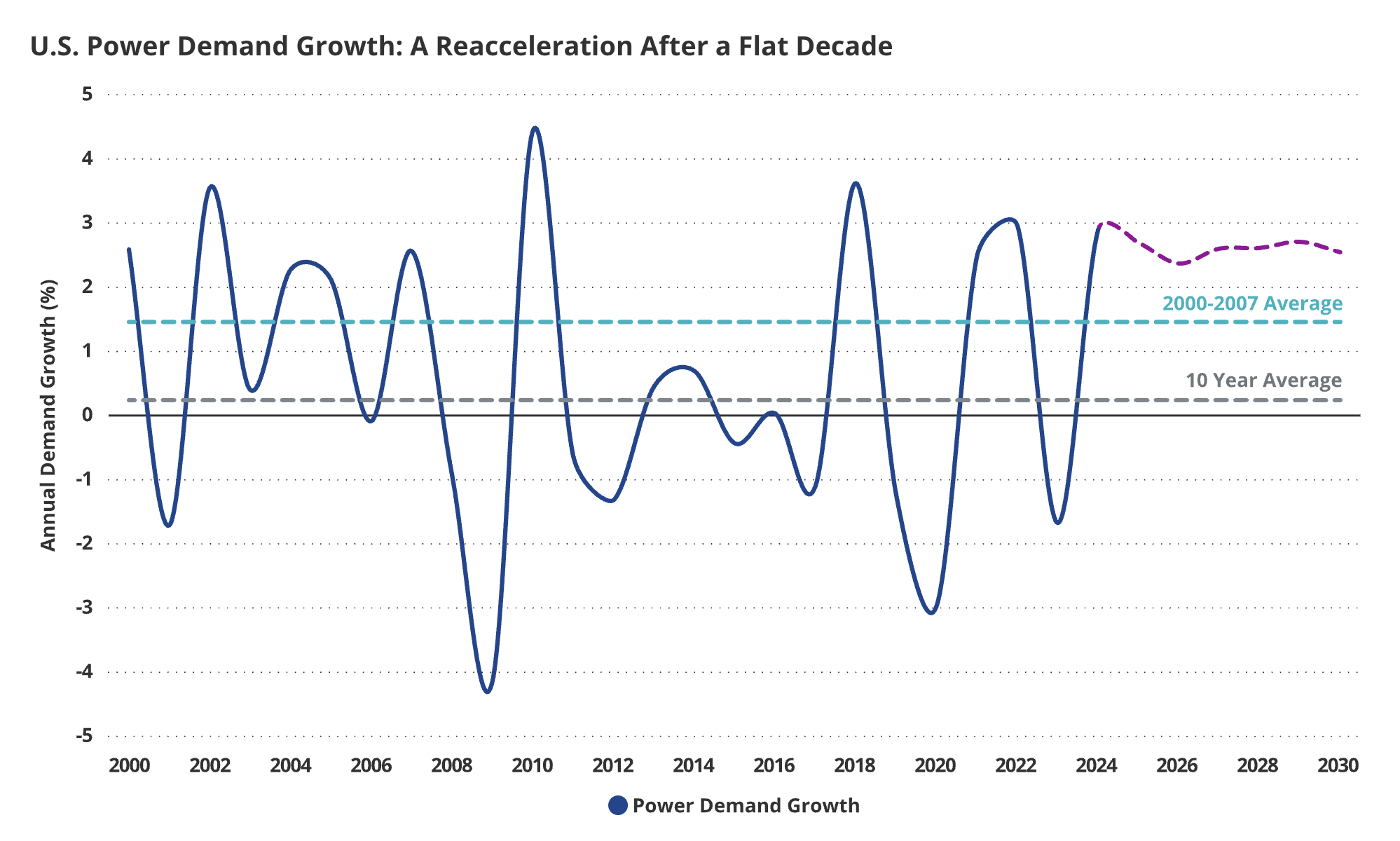

AI data centers, reshoring of manufacturing and broader electrification have ended about 20 years of flat U.S. electricity growth, raising grid reliability issues and renewed interest in nuclear.

Utilities, regional grid operators and federal agencies have revised electricity demand forecasts higher in recent years after roughly two decades of stagnant growth. Hyperscale AI facilities, expanding cloud infrastructure, industrial reshoring and wider electrification are cited as the main contributors to the shift.

Hyperscale data centers require concentrated, always-on power at specific sites. Those large continuous loads can create local stress on transmission and interconnection systems before national consumption figures fully reflect the change. Where transmission or interconnection capacity is limited, companies can face multi-year waits for service, a factor influencing choices about where new data centers and related facilities are built.

Federal incentives and industrial policy have supported announced projects in semiconductor fabs, electric vehicle plants and battery factories. Those facilities typically need sustained, high-volume electricity and tend to distribute demand across more regions than the data center footprint alone. Together with digital infrastructure growth, industrial projects have added to upward revisions in regional and national load forecasts.

Grid planners, large buyers and utilities are placing greater emphasis on reliability and dispatchability rather than solely on total megawatts. Many digital and industrial operations run continuously and are sensitive to brief interruptions, voltage variability or instability. Planning discussions now focus on delivering power at specific sites and times and on balancing variable renewable generation with firm generation, long-duration storage, transmission upgrades and demand-side flexibility.

Nuclear power has reappeared in planning conversations because of its steady output. U.S. nuclear plants show a capacity factor of about 93.1 percent, compared with roughly 33.5 percent for wind and 23.3 percent for solar, reflecting nuclear’s ability to provide continuous generation. Several large technology firms have pursued nuclear-sourced arrangements, including support for restarting a previously retired reactor and multi-year sourcing deals for cloud operations. Interest in next-generation designs such as small modular reactors has also increased. Nuclear projects continue to face long permitting and construction timelines, cost escalation risks, fuel cycle complexity and public acceptance issues. The current administration has announced actions intended to shorten approval processes and accelerate deployment; implementation and project execution will determine results.

Demand growth has amplified need for grid equipment, transformers, transmission components, cooling systems and power management gear for data centers, plus resilience tools such as backup generation and facility hardening. Supply-chain constraints for key components and long lead times for large equipment are factors that could affect the pace and location of capacity additions.

Electricity availability and reliability are influencing capital decisions across sectors that rely on continuous power. Market participants and planners are monitoring whether grid upgrades and new firm resources keep pace with concentrated load growth in specific regions.

Tags

Articles by this author