What is trade finance and how does it work?

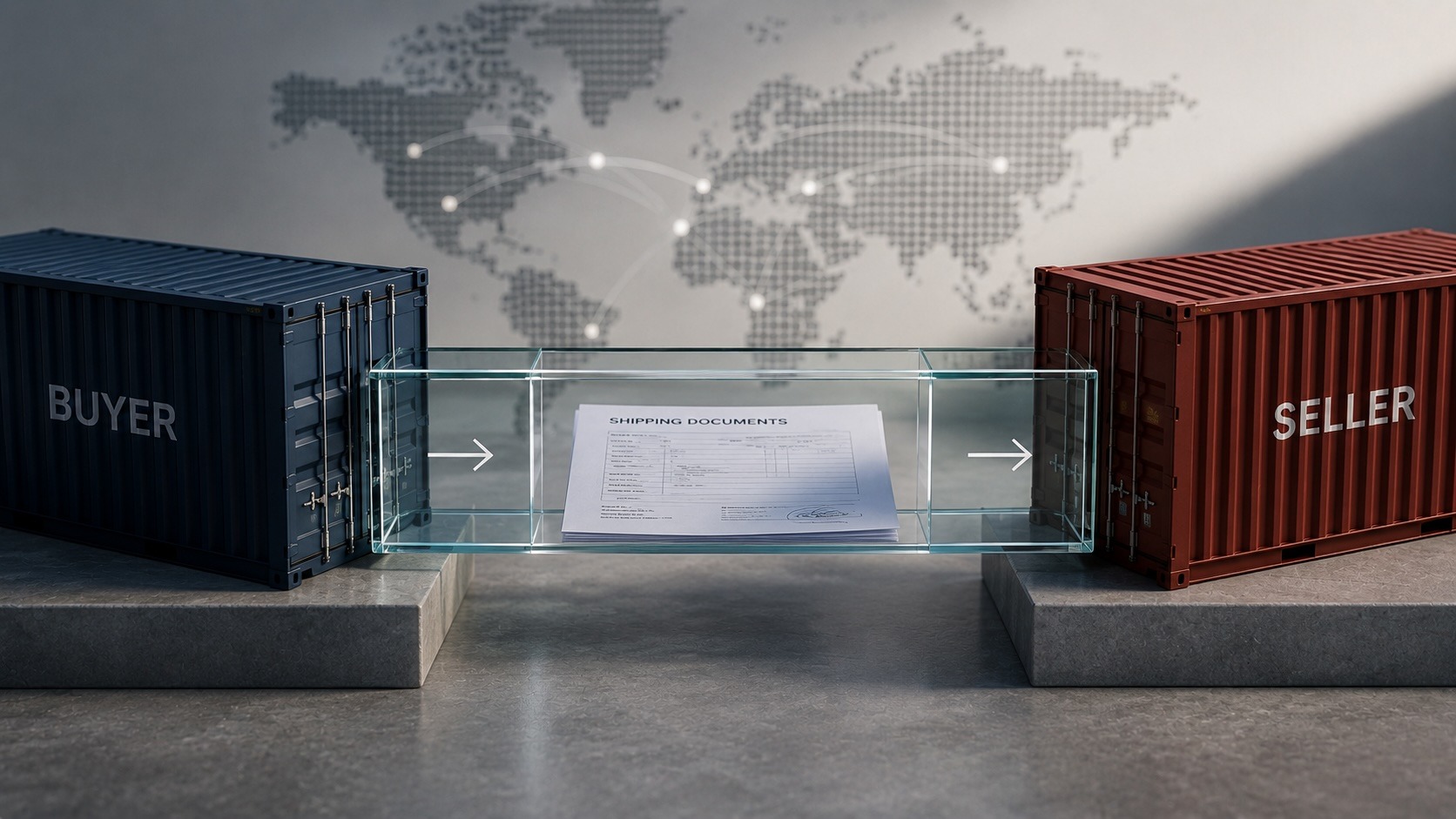

Every cross-border transaction carries a fundamental problem: the buyer wants to receive goods before paying, and the seller wants payment before shipping. Trade finance is the set of tools that resolves this standoff – and without it, a significant share of global commerce would simply not happen.

On this page

Whether a company is importing raw materials, exporting finished goods, or managing a supply chain that spans multiple countries, trade finance shapes how transactions are structured, how risk is allocated, and how cash flow holds up in the process.

What is trade finance?

Trade finance is a set of financial instruments and products that facilitate transactions between buyers and sellers, particularly across borders. It covers the financing, risk mitigation, and payment mechanisms that allow businesses to trade when transacting on open credit terms is not possible or practical.

Timing is where things get complicated. A manufacturer in Vietnam ships goods to a retailer in Germany. The goods are in transit for weeks. The retailer may not sell them for weeks more. Meanwhile, the manufacturer needs working capital to keep production running. Neither party wants to carry all the risk. Trade finance provides the structures that let both sides operate with reasonable certainty.

Banks and specialist financial institutions sit at the centre of most trade finance arrangements. They act as intermediaries, providing guarantees, credit, and payment mechanisms that give both sides of a transaction the assurance they need to proceed. In practice, this means a buyer can receive goods before funds clear, a seller can receive payment before the buyer pays, and both parties transfer a portion of their risk to a financial institution equipped to manage it.

Trade finance is not a niche product for large multinationals. Small and mid-sized businesses use it regularly whenever they operate across borders, deal in commodities, or work with suppliers or buyers who require structured payment terms.

Key instruments and solutions

Trade finance covers a broad range of instruments, each designed for different transaction types, risk profiles, and business relationships.

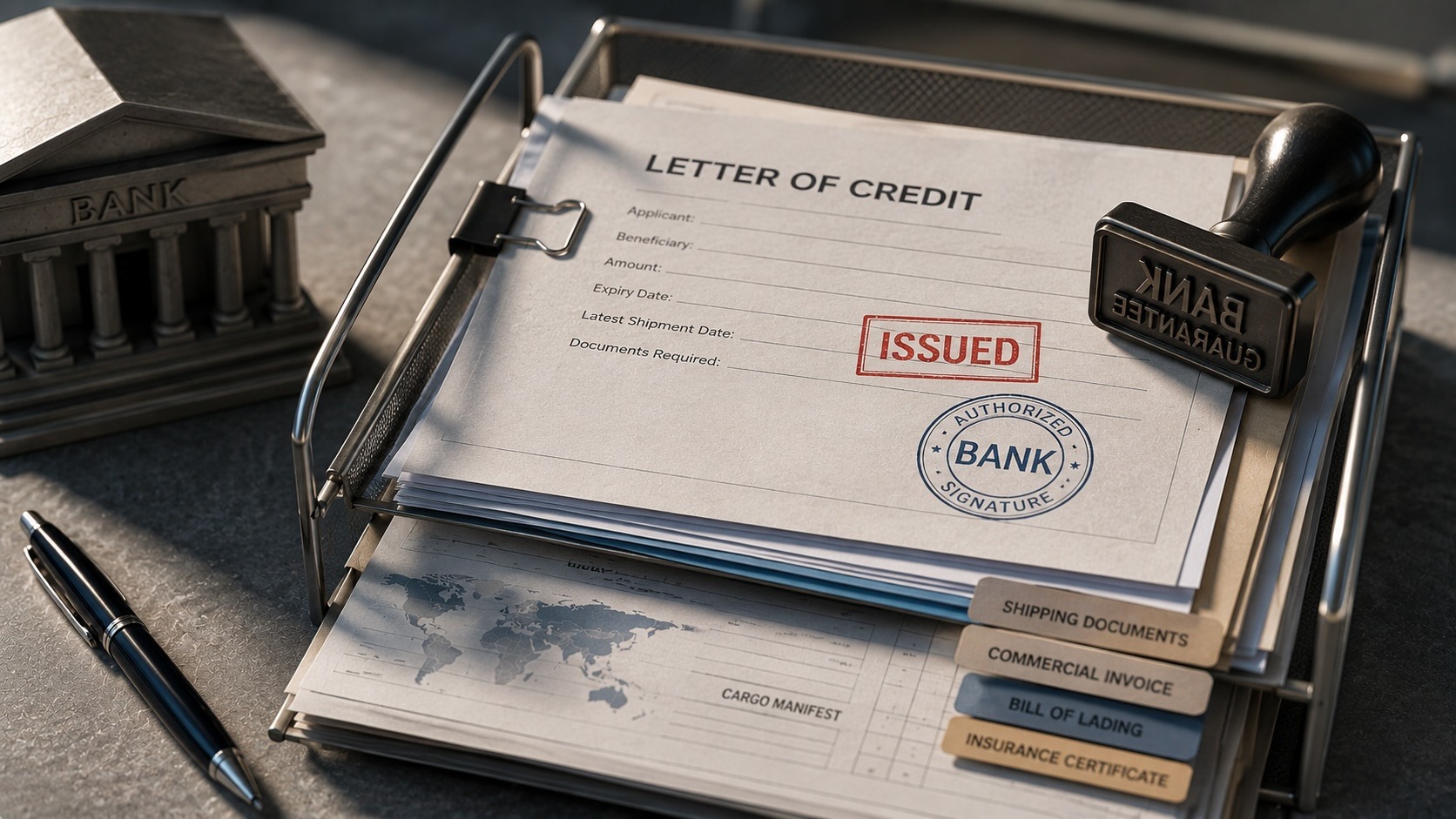

Letters of credit are among the most widely used tools. A letter of credit is a commitment from a bank on behalf of the buyer, guaranteeing payment to the seller once agreed conditions are met, typically presentation of shipping documents that confirm the goods have been dispatched as specified. The seller ships with confidence because the bank’s guarantee replaces the buyer’s promise. The buyer retains control because payment is conditional on documented performance.

Banks guarantee work on a related principle but serve a different function. Rather than facilitating payment, they protect against non-performance. If a contractor fails to deliver a project, or a buyer defaults on a purchase agreement, the guarantee ensures the affected party is compensated. They are common in construction, infrastructure, and large procurement contracts.

Documentary collections offer a lighter-touch alternative to letters of credit. The seller’s bank forwards shipping documents to the buyer’s bank with instructions to release them only against payment or acceptance of a bill of exchange. There is no bank guarantee involved, so the risk is higher for the seller, but the process is faster and cheaper, and it suits transactions where the parties have an established relationship.

Trade credit insurance protects exporters against the risk that a buyer fails to pay, whether due to insolvency, default, or political disruption in the buyer’s country. It allows businesses to extend credit to new markets and customers with more confidence, and it is often a prerequisite for obtaining trade finance from a bank.

Supply chain finance, sometimes called reverse factoring, allows buyers to extend payment terms to suppliers without those suppliers waiting longer for their money. The buyer’s bank pays the supplier early at a slight discount, and the buyer settles with the bank on its normal payment schedule. It strengthens supplier relationships and improves working capital on both sides.

Export financing and factoring give sellers access to cash against outstanding invoices, rather than waiting for buyers to pay. A business that invoices a buyer for $500,000 with 90-day terms can sell that receivable to a financial institution and receive most of the cash immediately. The cost is a fee or discount rate, but the benefit is working capital that does not sit locked in unpaid invoices.

Why trade finance matters

For most businesses, the practical case for trade finance starts with working capital. International transactions create timing mismatches: a company pays its supplier weeks or months before it collects from its buyer. Funding that gap from internal reserves or general credit lines is expensive and inefficient. Trade finance provides financing tied to the specific transaction, secured against the underlying goods or receivables, and structured around the actual trade cycle – which makes it cheaper and easier to scale than general borrowing.

Beyond cash flow, trade finance redistributes risk. Cross-border transactions introduce exposures that domestic commerce does not: currency fluctuation, political instability, unfamiliar counterparties, and regulatory differences across jurisdictions. Letters of credit and trade credit insurance allow businesses to transfer a significant portion of that exposure to institutions equipped to price and manage it, rather than absorbing it entirely on their own balance sheet.

Access to new markets is the less obvious but equally important benefit. Many buyers and sellers in emerging economies will not transact without structured payment guarantees. A letter of credit from a recognised bank signals credibility and provides the assurance that open account terms cannot. For exporters looking to expand beyond established relationships, trade finance is often what gets the first deal across the line.

At the macro level, the World Trade Organization estimates that 80 to 90 percent of global trade relies on some form of trade finance or credit. Disruptions to its availability, as seen during the 2008 financial crisis, have an immediate and measurable effect on the volume of goods moving across borders.

Final verdict

At its core, what is trade finance if not the infrastructure that makes international commerce work at scale – not by removing the risks of cross-border transactions, but by distributing them more efficiently between the parties best placed to manage them.

For businesses, understanding which instruments apply to which situations is a practical skill. A letter of credit is not interchangeable with a bank guarantee. Supply chain finance solves a different problem than export factoring. The right structure depends on the transaction, the counterparty, and the risk appetite of everyone involved.

As global trade continues to expand and businesses increasingly source, manufacture, and sell across multiple jurisdictions, trade finance will remain one of the more consequential tools in corporate financial management. Knowing how it works is the starting point for using it well.

Articles by this author