What are assets?

Every balance sheet starts with the same question – and most people assume they already know the answer. But the asset definition is deceptively simple: get it wrong, and everything downstream, from valuation to credit analysis to portfolio construction, gets murkier than it needs to be. Here is what assets actually are, how they are classified, and why the distinction between assets and liabilities matters more than it might seem.

On this page

What are assets?

An asset is anything you own or control that holds economic value or helps generate it. Cash in a money market account is an asset. So is a commercial property, a patent on a manufacturing process, a stake in a private equity fund, or the brand recognition a company has spent decades building.

Some assets hold value, some generate income, and some matter because they let a business operate in the first place. Many do more than one of those jobs at once.

Assets determine a company’s capacity to grow, absorb shocks, and attract capital. For individual smaller investors, they are the building blocks of net worth. For portfolio managers, the composition of an asset base shapes everything from risk exposure to long-term returns.

In accounting, assets appear on the left side of the balance sheet, offset by liabilities and equity. In practice, they are much more than a line item. A business with a strong, well-structured asset base can borrow more cheaply, reinvest more aggressively, and weather downturns more gracefully than one with a bloated liability stack and thin underlying assets. That matters whether the task is equity analysis, credit underwriting, or a potential acquisition review.

Understanding what qualifies as an asset is also the first step toward reading financial statements with confidence. With that distinction in place, it becomes easier to tell the difference between a company that merely looks healthy and one that actually is.

Understanding the main types of assets

Assets are grouped in different ways for a reason. Those distinctions affect valuation, liquidity, tax treatment, and risk.

Current vs. non-current assets is the most common accounting distinction. Current assets are expected to convert into cash within twelve months: cash and cash equivalents, accounts receivable, inventory, and short-term marketable securities. Non-current assets are held for longer periods and usually support operations over time: property, plant, equipment, and long-term investments. This split matters for liquidity analysis: a company with most of its value locked in non-current assets may be profitable on paper but constrained when it comes to meeting short-term obligations.

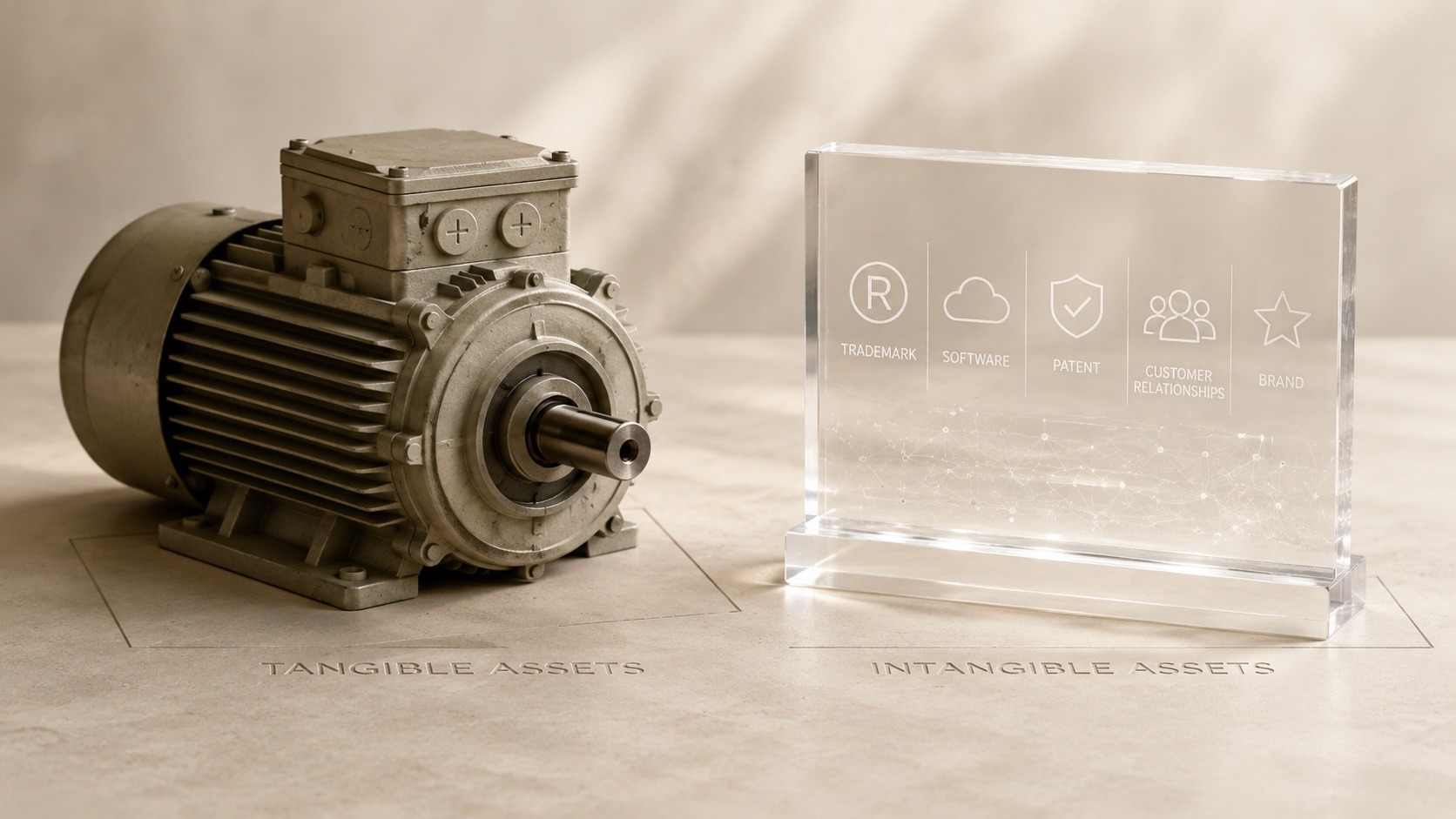

Tangible vs. intangible assets cut across a different dimension. Tangible assets have physical form: land, buildings, machinery, vehicles. They can be inspected, insured, and in many cases depreciated over a predictable useful life. Intangible assets are harder to see but often no less valuable. Patents, trademarks, software, customer relationships, and goodwill can represent the majority of enterprise value in technology, pharmaceutical, and consumer brand businesses. Overlooking intangibles is a common mistake in financial analysis.

Financial assets such as stocks, bonds, derivatives, and bank deposits derive their value from a legal or contractual claim rather than physical substance. They are the primary domain of capital markets and institutional portfolio management. Real assets including real estate, commodities, infrastructure, and timberland offer different return profiles, often with lower correlation to public markets and stronger inflation protection. Sophisticated allocators typically hold both.

Digital assets add a newer and still-evolving layer. Cryptocurrencies, tokenized securities, and blockchain-based instruments have moved from the fringe toward the mainstream of institutional consideration, even as accounting treatment and regulatory frameworks continue to develop unevenly across jurisdictions.

Different asset types carry different depreciation schedules, tax treatment, reporting requirements, and valuation methodologies. A real estate asset is not valued the same way as a technology patent or a government bond, and conflating them can lead to serious mispricing.

Assets vs liabilities: what’s the difference?

The easiest way to clarify the concept is to set assets against liabilities. The assets vs. liabilities distinction is foundational in finance: assets represent what you own or control; liabilities represent what you owe.

Liabilities are obligations: loans, mortgages, accounts payable, lease commitments, deferred revenue. They sit on the right side of the balance sheet and reduce what ultimately belongs to shareholders or owners. Net worth, or equity, is what remains after liabilities are subtracted from total assets. That figure is a far more meaningful indicator of financial health than gross asset value alone.

A concrete example: a property worth $600,000 financed by a $520,000 mortgage leaves $80,000 in actual equity. The property is valuable, but the owner’s real equity is limited. The same logic applies at the corporate level. A company may report $5 billion in total assets while carrying $4.5 billion in debt. The balance sheet looks substantial until you account for what is owed.

That is why balance sheet analysis does not stop at the asset column. Leverage ratios, debt coverage metrics, and asset quality reviews exist precisely to assess how liabilities interact with assets over time. A high asset base paired with high-quality, long-duration liabilities can be entirely manageable. The same asset base paired with short-term, high-cost debt in a rising-rate environment can look much less stable.

Lenders and credit analysts look at this relationship carefully. Assets can serve as collateral, but what matters more is whether cash flows from those assets are sufficient to service obligations, and by what margin. Investors pricing equity do the same: enterprise value, net asset value, and book value metrics all require understanding both sides of the balance sheet simultaneously.

Asset quality also matters independently of size. Not all assets on a balance sheet are equally reliable. Some may be difficult to liquidate, some may be overvalued relative to market, and some — like goodwill from an acquisition — may need to be written down if business conditions change. A strong asset base is not just a large one; it is one whose value holds up under scrutiny.

Final takeaway

The question of what is an asset sounds basic enough to answer in a sentence. In practice, the concept sits at the center of nearly every financial judgment worth making.

For investors, understanding what an asset is, how it is categorized, valued, and reported, is not separate from analysis. It sits at the center of it. The difference between a well-capitalized business and one quietly heading toward distress often lies precisely in asset quality, asset composition, and how assets are positioned against liabilities.

For portfolio managers, asset classification shapes allocation strategy, risk assessment, and performance attribution. Knowing whether you are looking at a financial asset, a real asset, or an intangible one changes how you model it, stress-test it, and price it.

And for anyone reading a balance sheet, whether to assess a potential investment, evaluate a counterparty, or understand their own financial position, the asset definition is where that analysis starts. Get that definition right, and the rest of the balance sheet is easier to read.

Articles by this author